2.png)

- Top

- IR

- To Individual Investors

- President interview

- Interview with the President for the FY2021

We will promote company-wide efforts to build a management foundation that can overcome changes in the business environment.

Interview with the President for the FY2021

Q: Looking back on the FY2021, please give us an overview of the business situation.

Suzuki:

Recovery from the slump in the previous fiscal year. Sales expanded mainly in the automotive and industrial markets.

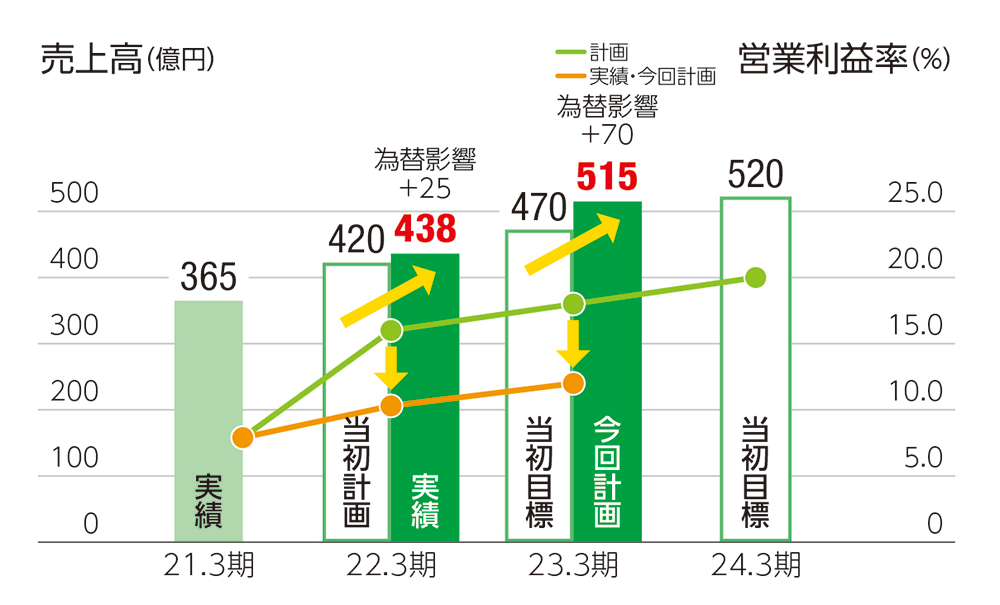

In this fiscal year, sales recovered from the decline in the previous fiscal year, which was significantly affected by the new coronavirus infection, and grew mainly in the automotive and industrial markets, while the weak yen also contributed to record sales. Profits also improved significantly due to higher capacity utilization and efforts to reduce costs and fixed costs. However, from the second quarter onward, the supply of semiconductors and other components tightened, and the impact of soaring raw material prices and transportation costs, as well as supply chain disruptions, spread, resulting in profit levels lower than initially planned.

In the mainstay automotive market, the powertrain field continued to perform well, driving growth in sales in Japan, China, and South Korea. The infotainment and safety fields also started to recover. Sales in the powertrain field increased by approximately 90% year-on-year, indicating strong demand for xEV . Our original anti-vibration solution service for powertrain equipment was also successful, contributing to the acquisition of orders. On the other hand, due to the impact of the shortage of semiconductors, sales fell short of the original sales plan by approximately 3 billion yen.

In the consumer market, demand for game consoles and OA equipment for working from home increased amid the ongoing COVID-19 environment. Despite being affected by the shortage of semiconductors from the third quarter onward, sales remained strong and achieved the initial sales plan. The industrial market performed well throughout the year, achieving a 70% year-on-year increase in sales. In particular, demand for capital investment in China led to an increase in sales for FA equipment, and new installations for 5G base stations in the telecommunications field also contributed.

As a result of the above, the consolidated results are as follows: sales of 43,863 million yen (up 20.1% year-on-year), operating income of 4,520 million yen (up 55.9% year-on-year), ordinary income of 4,838 million yen (up 62.9% year-on-year) ), and profit attributable to owners of parent was 3,913 million yen (an increase of 82.7% year on year).

Q: Please tell us about the future development of the medium-term management plan.

Suzuki:

Due to changes in the environment, there is a delay in our profit plan, but we will rebuild our management foundation over the next two years.

The Company has set a long-term vision aiming for sales of 100 billion yen by the FY2029. We are promoting. As of a year ago, the negative impact of the COVID-19 pandemic on the business environment was lower than expected, and the automobile market in particular showed a rapid recovery. In fact, in the first year of the plan, as mentioned above, the automotive market centered on the powertrain field performed well, and sales increased significantly. However, the trend of re-expansion of infectious diseases, short supply of semiconductors, and soaring raw material prices, as well as the rising geopolitical risk from the situation in Ukraine, have made it necessary to revise the global automobile production volume forecast, which is the premise of the plan. We estimate that while xEVs (electric vehicles) will remain strong in the future, due to the stagnation of non-xEVs, global production in FY2022 will be 78 million units, almost the same level as in FY2021, which is significantly lower than the previous forecast of 92 million units.

As for the impact on the medium-term management plan, in FY2022, the second year of the plan, net sales are expected to exceed the initial plan due to the expansion of the powertrain field and the depreciation of the yen, but operating income margin is expected to fall short of the initial plan due to the expected increase in costs, including lower capacity utilization and higher raw material and transportation costs. In FY2023, the final year of the plan, we expect the severe external environment to continue, including lower global automobile production volume and higher raw material and transportation costs compared to the initial plan, and we will continue to rebuild our management foundation by improving our cost structure and strengthening supply chain management.

Specifically, we intend to ensure cost competitiveness to outperform soaring raw material and transportation costs by reviewing pricing policies, reducing the cost of mainstay products, improving factory utilization and productivity, and reforming total distribution costs. At the same time, we will strengthen our supply chain management by stabilizing our production system, promoting local production for local consumption, and renovating our ERP system.

Q: What is your outlook for the FY2022?

Suzuki:

While expanding sales, we will work to improve our profit structure and strengthen our supply chain management.

Although we expect FY2022 profits to fall short of the mid-term management plan due to the factors mentioned above, the powertrain segment will continue to drive sales growth, and we expect to achieve the final year target of the mid-term management plan for this segment one year ahead of schedule. We will strive to capture the growth of xEV in the automotive market and the high demand in the industrial equipment and communication fields in the industrial market, and strive to improve our profit structure and strengthen supply chain management while expanding sales. .

Capital investment for the FY2022 is expected to reach a record high of 9 billion yen due to an increase in investment related to the renovation of the ERP system, the new factory to be built in Akita Prefecture, and the production side of the mold manufacturing subsidiary. .

Based on the above assumptions, the consolidated results are as follows: net sales of 51.5 billion yen (up 17.4% year on year), operating income of 6.16 billion yen (up 36.3% year on year), ordinary income of 6.2 billion yen (up 28.1% year on year), parent company shareholders We forecast net income attributable to owners of the parent of 4.5 billion yen (up 15.0% year on year).

Q: Do you have a message to your shareholders?

Suzuki:

We will realize our “ideal state”, increase our corporate value, and make a greater contribution to society.

In line with our shareholder return policy of maintaining stable dividends with a dividend payout ratio of 30% or more, we decided to pay a year-end dividend of 60 yen per share (an increase of 10 yen year-on-year) as planned. The year-end dividend for the FY2022 is scheduled to be ¥60. Going forward, in order to achieve ROE of over 10%, as set forth in our long-term vision, we will further enhance shareholder returns through measures such as raising the level of dividends and repurchasing treasury stock, while taking into account the balance with securing investment funds for growth. We intend to proactively review our capital policy in order to achieve this.

In our medium-term management plan, we have set ourselves the goal of being “No.1 in the industry, customer first,” and in our long-term vision, we aim to be “ranked within the top 10 of the world's connecting parts industry.” We will realize these ideals, increase our corporate value, and make greater contributions to society. We would like to ask our shareholders to look forward to the further development of our business and to continue to provide us with your long-term support.